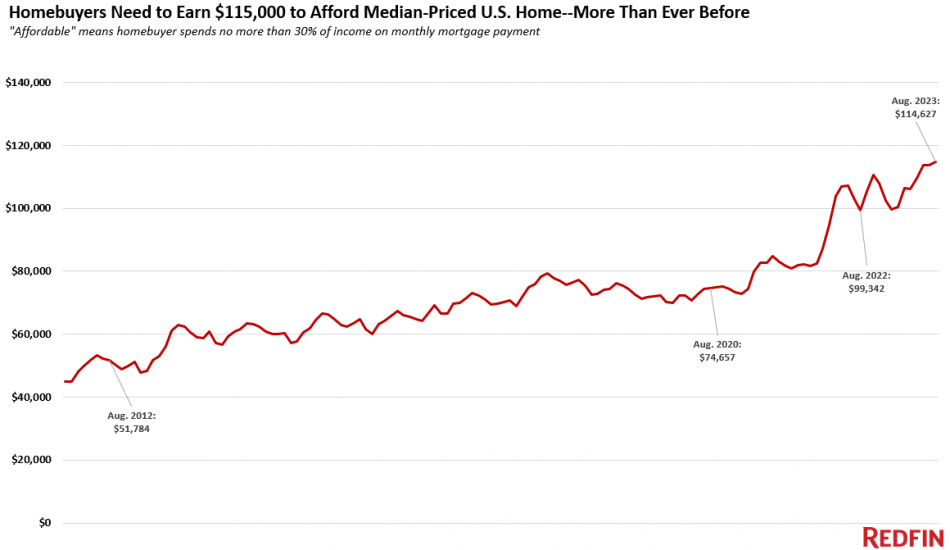

A homebuyer must earn $114,627 to afford the median-priced U.S. home, up 15 percent from a year ago and up more than 50 percent since the start of the pandemic, according to Redfin. That’s the highest annual income necessary to afford a home on record. Couple that with the fact that interest rates are now at 8 percent and it’s no wonder that this year is likely to be the slowest for residential real estate since 2008.

Redfin estimates that this year is likely to end with roughly 4.1 million existing home sales nationwide, the fewest since the proverbial bubble burst.

Buyers in the Bay Area country–the most expensive markets in the country–must earn more than $400,000 to afford the median-priced home in the area. That up nearly 25 percent year-over-year. The next five metros requiring the highest income are all in California: Anaheim ($300,000), Oakland ($250,000), San Diego ($241,000), Los Angeles ($237,000) and Oxnard ($233,000).

The typical U.S. homebuyer’s monthly mortgage payment is at an all-time high of $2,866, up 20 percent from $2,395 a year earlier.

“In a homebuyer’s ideal world, rising mortgage rates would push demand and home prices down enough to make up for high interest payments. But that’s not what’s happening now: Although new listings are ticking up slightly, inventory is still near record lows as homeowners hang onto their low mortgage rates—and that’s propping up prices,” said Redfin Economics Research Lead Chen Zhao. “Buyers—particularly first-timers—who are committed to getting into a home now should think outside the box. Consider a condo or townhouse, which are less expensive than a single-family home, and/or consider moving to a more affordable part of the country, or a more affordable suburb.”

![[Valid RSS]](https://californialistings.com/wp-content/uploads/2021/03/valid-rss-rogers.png)

{kind=link}