Rent hikes continued around the country last month, with new numbers from Redfin marking monthly and annual records.

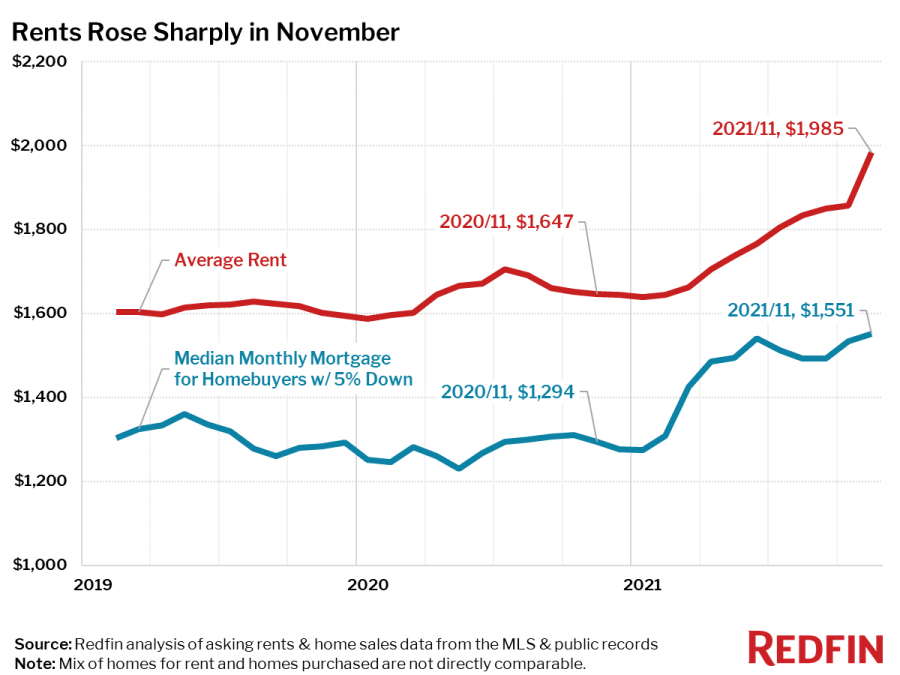

According to Redfin, average monthly rents increased 21 percent nationwide over the past year and 7 percent between October and November 2021, the highest annual and monthly growth rates in at least two years—as far back as Redfin’s rental data goes.

Rent-price increases outpaced mortgage payment increases for new homebuyers in 19 of the 50 largest metro areas in the U.S. during November.

“First inflation came for the for-sale housing market, and now it is coming for the rental market,” said Redfin Chief Economist Daryl Fairweather. “Many people have been priced out of the for-sale market and are looking to rent instead, but that demand is pushing up rents. Anyone who bought a home before this year can pat themselves on the back because their mortgage payments are fixed, meaning their biggest recurring expense is immune to inflation. If you are looking to buy or rent now, there’s nowhere to hide from inflation when it comes to housing costs. The good news is that the tight labor market means it’s a great time to move somewhere more affordable. Chances are good that no matter where you go, you’ll be able to find a new job relatively quickly.”

California managed to stay out of the top 10 metro areas with the fastest-rising annual rents, with New York and Florida heavily represented. The only two metro areas that saw rent declines, according to Redfin, were Kansas City and St. Louis.

Top 10 Metro Areas With Fastest-Rising Rents Year Over Year

- Miami, FL (35 percent)

- Fort Lauderdale, FL (35 percent)

- West Palm Beach, FL (35 percent)

- New York, NY (34 percent)

- Newark, NJ (34percent)

- Nassau County, NY (34 percent)

- New Brunswick, NJ (34 percent)

- Jacksonville, FL (33 percent)

- Austin, TX (30 percent)

- Tampa, FL (28 percent)

![[Valid RSS]](https://californialistings.com/wp-content/uploads/2021/03/valid-rss-rogers.png)

{kind=link}