First-time buyers heading into the market better have had a raise in the last 12 months—or successfully played the lottery—as Redfin is out with some discouraging news. A first-time homebuyer must earn roughly $64,500 per year to afford the typical U.S. “starter” home, up $7,200 from a year ago.

The culprit? A one-two punch of higher mortgage rates and higher home prices. A person looking to buy a typical starter home today would have a monthly mortgage payment of $1,610, up 13 percent from a year ago and nearly double the typical payment just before the pandemic.

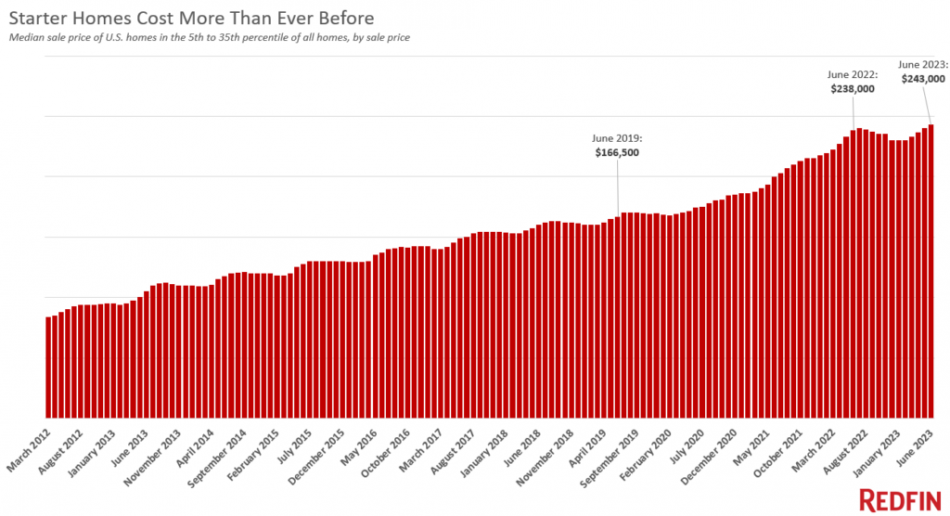

As noted in the report, the typical starter home sold for $243,000 in June, up 2.1 percent from a year earlier and up more than 45 percent from before the pandemic. Average mortgage rates hit 6.7 percent in June, which is up from 5.5 percent the year before and just under 4 percent before the pandemic.

“Buyers searching for starter homes in today’s market are on a wild goose chase because in many parts of the country, there’s no such thing as a starter home anymore,” said Redfin Senior Economist Sheharyar Bokhari. “The most affordable homes for sale are no longer affordable to people with lower budgets due to the combination of rising prices and rising rates. That’s locking many Americans out of the housing market altogether, preventing them from building equity and ultimately building lasting wealth. People who are already homeowners are sitting pretty, comparatively, because most of them have benefited from home values soaring over the last few years. That could lead to the wealth gap in this country becoming even more drastic.”

San Francisco, Austin and Phoenix are the only major U.S. metros where the income needed to buy a starter home has dropped over the last year. A homebuyer in San Francisco must earn $241,200 to afford the typical “starter” home, down 4.5 percent, or $11,300, from a year earlier. Austin buyers must earn $92,000, down 3.3 percent year-over-year, and Phoenix buyers must earn $86,100, down about 1 percent.

Starter-home prices are down year-over-year in a number of West Coast markets, including San Jose, Sacramento, Oakland, Los Angeles, Anaheim, San Diego and Riverside.

![[Valid RSS]](https://californialistings.com/wp-content/uploads/2021/03/valid-rss-rogers.png)

{kind=link}