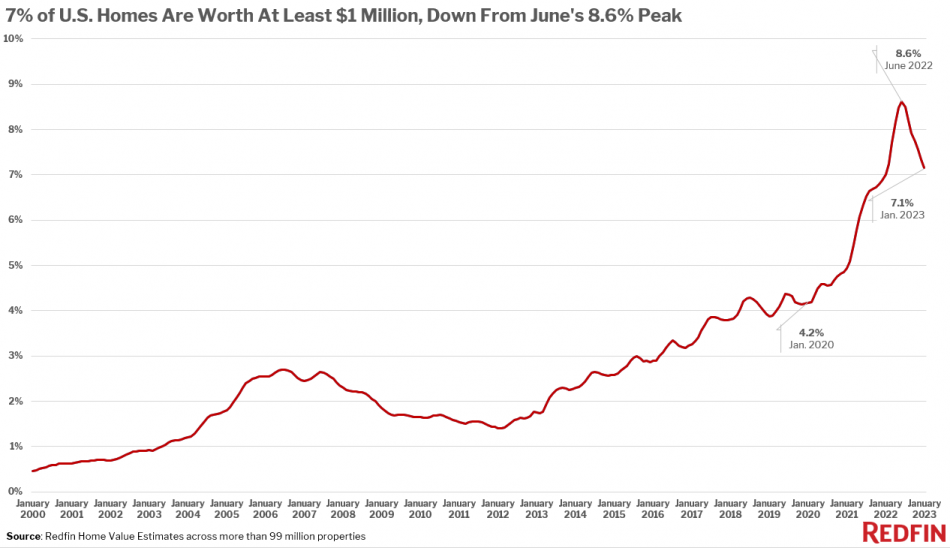

The slow descent of home values in the U.S. has begun showing up in a somewhat unexpected place: the decline of million-dollar inventory.

According to Redfin, just over 7 percent of U.S. homes are worth $1 million or more. That’s down from June 2022’s all-time high of 8.6 percent and essentially unchanged from a year ago–but it’s up from 4.2 percent just before the pandemic began.

As home values have dropped from record highs, that has pushed a certain portion of homes that would have been worth seven figures at the peak of the pandemic homebuying frenzy below the million-dollar threshold.

The share of homes valued at seven figures is falling quickest in the Bay Area. More than 80 percent of San Francisco homes are worth at least $1 million–the biggest share of the 99 most populous U.S. metros, but down from 86.3 percent a year ago.

Oakland’s share of million-dollar homes stands at 44.8 percent, down from 50 percent a year ago. That’s followed by Seattle (27.5 percent, down from 30.9 percent), New York (29.5 percent, down from 32.5 percent) and San Jose (79.2 percent, down from 81.7 percent).

“Home values are coming down from their peak and fewer sellers could fetch seven figures–but that doesn’t mean buyers are getting a break,” said Redfin Economics Research Lead Chen Zhao. “The typical homebuyer’s monthly mortgage payment is even higher than it was when home values peaked in the spring because rates are so much higher and although home prices have come down, they certainly haven’t crashed. Now isn’t the time for buyers who need to take out a loan to get a good deal: Buying an $800,000 home today would cost more per month than buying a million-dollar home a year ago.”

![[Valid RSS]](https://californialistings.com/wp-content/uploads/2021/03/valid-rss-rogers.png)

{kind=link}