By now, most real estate talking heads have made it perfectly clear on cable news that this is no early 2000s housing bubble and that we shouldn’t expect a burst. But what goes way up naturally has to come down at some point—and we may be seeing the early signs of a settling market.

According to new data from Redfin, both pending sales and asking prices began to decline or flatten in the four weeks ending May 30.

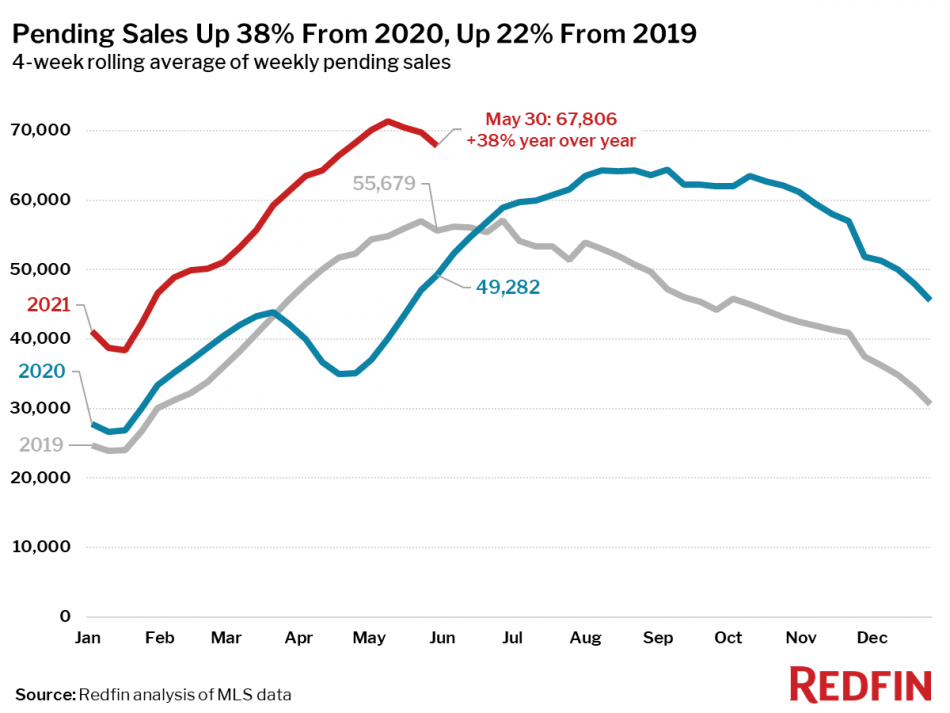

In addition to the previously reported dip in mortgage interest, pending home sales fell 3 percent from the four-week period, compared to a 2 percent increase over the same period in 2019. Compared to 2020, at the start of the pandemic, however, pending sales were up 38 percent.

Redfin also notes that asking prices fell $2,500 from the four-week period ending May 23 to a median of $354,975. That’s still up 11 percent from the same period in 2020. New listings were down 8 percent from the same period in 2019 (again, Redfin analysts left the 2020 time period out considering it was early pandemic).

And finally, active listings fell 37 percent from the same period in 2020.

“The housing market was going 100 miles per hour and now it’s down to 80,” said Redfin Chief Economist Daryl Fairweather. “This is not the bursting of a bubble. Rather, it’s a sign that consumers might rather spend their time and money on other things besides housing now that travel, dining and entertainment are resuming in full force.”

![[Valid RSS]](https://californialistings.com/wp-content/uploads/2021/03/valid-rss-rogers.png)

{kind=link}