The Data & Analytics division of Black Knight, Inc. has released its latest Mortgage Monitor Report, highlighting a topsy-turvy June in residential real estate.

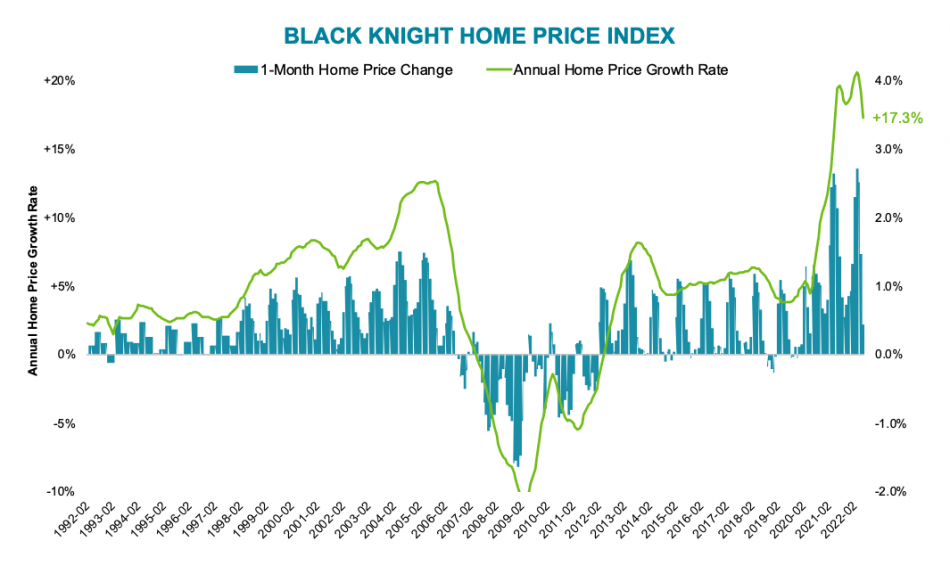

Annual home price growth dropped by nearly two percentage points in June—19.3 percent to 17.3 percent—marking the greatest single-month slowdown on record since at least the early 1970s. According to Black Knight, the rate of slowing jumped 66 percent from May.

At the same time, the decline coincides with the largest single-month gain in homes listed for sale in 12 years. Black Knight’s Collateral Analytics data shows a seasonally adjusted 22 percent increase in the number of homes listed for sale over the past two months.

Inventory, however, is still 54 percent below 2017-2019 levels. The report notes that it would take more than a year of such record increases for inventory levels to fully normalize, making up for the national shortage of 716,000 listings.

“The pullback in home price growth in June marked the strongest single month of slowing on record dating back to at least the early 1970s—and it wasn’t even close,” said Black Knight Data & Analytics President Ben Graboske. “For context, during the 2006 downturn the strongest single-month slowing was 1.19 percentage points—about what we saw last month—and June topped that by 66 percent. The slowdown was broad-based among the top 50 markets at the metro level, with some areas experiencing even more pronounced cooling. In fact, 25 percent of major U.S. markets saw growth slow by three percentage points in June, with four decelerating by four or more points in that month alone.”

On a local level, the report finds the average San Jose home value has fallen 5.1 percent (-$75,000) in the last two months alone, marking the sharpest pullback from recent highs among the top 50 U.S. markets. Seattle follows with a 3.8 percent decline, a reduction of more than $30,000. San Francisco home values have dropped by 2.8 percent or $35,000, over the same time period.

San Diego and Denver round out the top five, falling 2 percent and 1.4 percent, respectively. In total, prices have pulled back from recent peaks in 12 of the 50 largest markets, with seven pulling back by 1 percent or more.

“Still, while this was the sharpest cooling on record nationally, we’d need six more months of this kind of deceleration for price growth to return to long-run averages,” Graboske. said. “Given it takes about five months for interest rate impacts to be fully reflected in traditional home price indexes we’re likely not yet seeing the full effect of recent rate spikes, with the potential for even stronger slowing in coming months.”

![[Valid RSS]](https://californialistings.com/wp-content/uploads/2021/03/valid-rss-rogers.png)

{kind=link}