“Balance” is quickly becoming the go-to term for market experts this Summer. While prices and mortgage rates remain high, changes in inventory and a slower sales pace are bringing balance to a red hot sellers market.

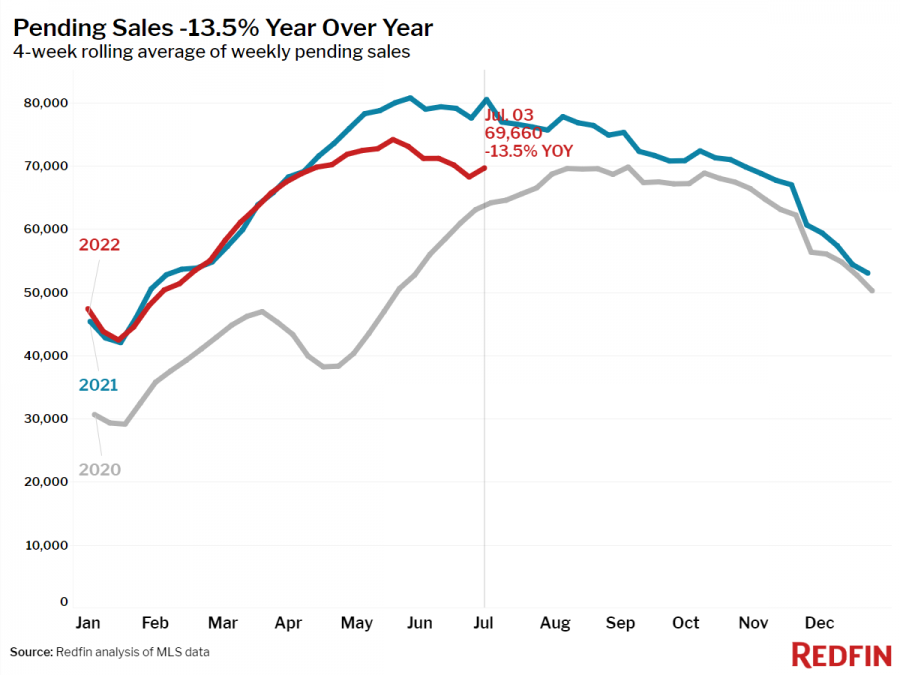

The latest data out from Redfin points to even more changes, with pending home sales down 13 percent nationally for the week ending July 3. The drop marks the largest decline since May 2020.

New listings of homes for sale were down 1.4 percent from a year earlier. Active listings (the number of homes listed for sale at any point during the period) fell 2 percent year over year—the smallest decline since October 2019.

“Conditions for homebuyers are improving. Housing remains expensive, but mortgage rates just posted their biggest weekly drop since 2008, which makes buying a home a bit more affordable,” said Redfin chief economist Daryl Fairweather. “One way buyers can take advantage of the shift in the market is seeking concessions from sellers. That could include asking the seller to buy down your mortgage rate, pay for repairs or cover some of your closing costs.”

According to Redfin, the median home sale price was up 13 percent year-over-year to $396,000. This growth rate is down from the March peak of 16 percent.

The median asking price of newly listed homes increased 15 percent year-over-year to $399,973, but was down 2.1 percent from the all-time high set during the four-week period ending June 5.

On average, 7 percent of homes for sale each week had a price drop, a record high as far back as the data goes, through the beginning of 2015.

![[Valid RSS]](https://californialistings.com/wp-content/uploads/2021/03/valid-rss-rogers.png)

{kind=link}